Linda Larsen

Linda Larsen

Table of Contents

The ground shifted under American crypto traders in 2026. Form 1099-DA — the IRS’s new digital-asset reporting instrument — now requires brokers to report cost basis on transactions effected on or after January 1, 2026, meaning every swap on a custodial US exchange generates a fuller paper trail that goes directly to the IRS. Simultaneously, the FTX bankruptcy and criminal fraud conviction reminded millions of users what happens when a centralized platform collapses around their funds. The SEC’s enforcement actions against former FTX executives sent a clear message that securities fraud in crypto carries real career-ending consequences.

The result? A bifurcated market. On one side: regulated, identity-verified, tax-reporting platforms that give you fiat on-ramps and institutional security. On the other: non-custodial swap platforms and decentralized alternatives that preserve the original privacy promise of crypto while still operating within legal boundaries.

Neither side is wrong. They serve different needs, risk tolerances, and use cases. This guide maps both, so you can pick the right tool for your situation — and avoid the landmines in between.

Comparison Table: 10 Best Places to Buy Crypto in the USA (2026)

| Platform | KYC Required | Fiat On-Ramp | Custody Model | Best For |

|---|---|---|---|---|

| Godex.io | None | No (crypto only) | Non-custodial | Instant crypto swaps |

| Bisq | None | Yes (P2P fiat) | Non-custodial | Privacy advocates (BTC) |

| MEXC | Optional (tiered) | Limited | Custodial (offshore) | Altcoin traders |

| Coinbase | Full | Yes (USD) | Custodial | Regulated first-timers |

| Kraken | Full | Yes (USD) | Custodial | Security-focused traders |

| Gemini | Full | Yes (USD) | Custodial | Institutional buyers |

| Robinhood | Full | Yes (USD) | Custodial | Stock investors adding BTC/ETH |

| Crypto.com | Full (tiered) | Yes (USD) | Custodial | Rewards seekers, card users |

| Cash App | Full | Yes (USD) | Custodial | BTC-only DCA buyers |

| Bitcoin ATMs | Minimal (<$1K) | Yes (cash) | Non-custodial | Unbanked / cash buyers |

Why “Best Exchange” Is the Wrong Question in 2026

The better question is: best for what?

A retiree converting USD into Bitcoin for the first time needs something different from a DeFi-native trader moving between chains at 2 a.m. The compliance climate matters enormously here. The regulatory picture shifted decisively in 2025: the SEC dropped dozens of crypto cases, disbanded its National Cryptocurrency Enforcement Team, and refocused on outright fraud rather than grey-area violations. That pivot created more breathing room for legitimate platforms — but it also left the landscape messier. Many offshore platforms have quietly geo-blocked American IPs to avoid future scrutiny. Others have added mandatory KYC tiers mid-operation, surprising users who signed up expecting anonymity.

Six questions worth asking about any platform before you commit:

- Custody model — does the platform hold your keys, or do you?

- Regulatory status — licensed in the US, offshore, or decentralized?

- KYC requirements — none, light, or full identity verification?

- Fiat access — can you deposit dollars directly?

- Tax reporting — will it generate a 1099-DA, and how does that affect you?

- Fee structure — spread, flat fee, or percentage commission?

With those filters in mind, here are the ten best places to buy crypto in the USA right now.

Non-Custodial & No-KYC Platforms

These three platforms require no identity verification and hold no long-term custody of your funds. They represent different implementations of the same principle: crypto transactions that don’t require you to prove who you are. The trade-off, across all three, is that there is no account to recover, no support team with access to your funds, and no 1099-DA to make tax season easier.

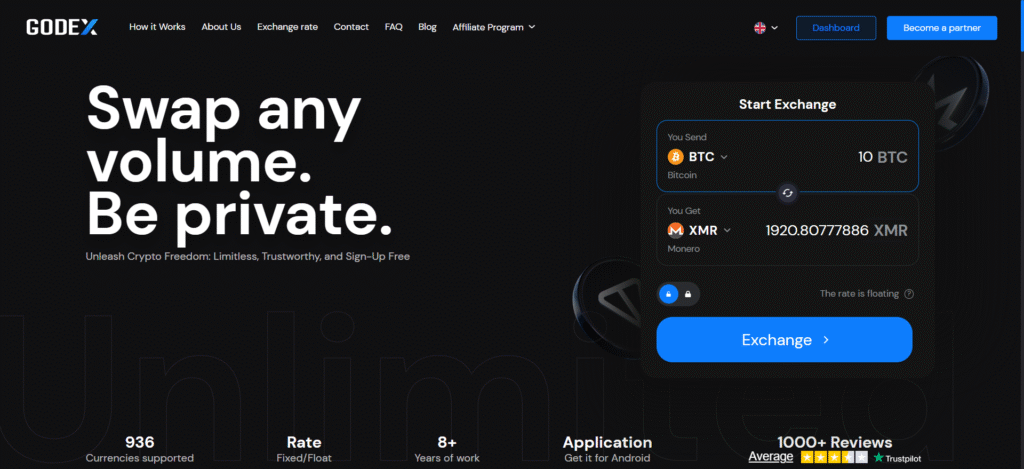

1. Godex — Instant Non-Custodial Swaps, No Registration

Godex is not a place to buy crypto with dollars — it’s where you go once you already have crypto and want to swap it instantly, anonymously, and without handing over your identity documents. Godex covers the full trading spectrum: BTC and ETH pairs for everyday swaps, privacy coins like Monero and Zcash that most regulated exchanges have quietly delisted, the major altcoins (SOL, XRP, ADA, AVAX), and a deep bench of niche tokens that rarely appear on US-regulated platforms. Fixed and floating rate options, no upper limit on swap volume, zero personal data collected. No registration, no email, no KYC — ever.

The workflow is clean: choose your pair, enter your destination wallet address, send your deposit. Funds go directly to your receiving wallet; Godex holds them only for the duration of the swap itself — there is no account balance, no custodial relationship.

Under current IRS guidance, this model is generally not the type of arrangement that triggers mandatory broker reporting obligations. The platform does not generate a Form 1099-DA on your behalf, though users remain responsible for self-reporting gains and a tax professional can advise on specifics.

Who it’s for: Existing crypto holders who want to swap quickly without leaving identity traces; anyone needing privacy coin conversions; high-volume traders who hit limits elsewhere.

Key facts:

- BTC, ETH, privacy coins (XMR, ZEC), major altcoins, and hundreds of niche tokens — all in one place

- Fixed-rate and floating-rate options

- No registration, no email, no KYC

- No upper swap limits

- Non-custodial account model — no balances held between transactions

- Orders deleted after two weeks; no long-term data retention

- Years of continuous operation with an impeccable online reputation — Trustpilot review volume is exceptionally high for the instant-swap category and the rating has remained strong, which is difficult to maintain or fabricate at scale

- Partnerships with privacy-first industry leaders including Trezor, Monero, and Edge Wallet

Limitation: Crypto-to-crypto only — no fiat on-ramp; not a trading terminal with charts or order books. Available globally; users should review Godex’s current Terms of Service for jurisdiction-specific availability before transacting.

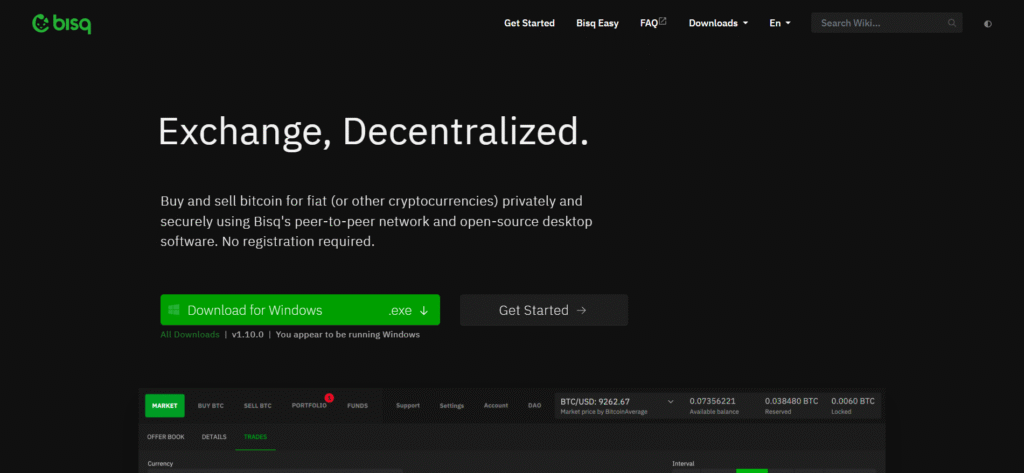

2. Bisq — Truly Decentralized Peer-to-Peer

Bisq is the most privacy-preserving way to buy Bitcoin in the United States — a fully decentralized, open-source peer-to-peer trading network with no central servers, no corporate entity, and no KYC requirement. DEX platforms like Bisq remain legal in US territories because they operate as protocols rather than traditional exchanges.

Trades on Bisq match buyers and sellers directly. Dispute resolution runs through a decentralized arbitration system. You download the desktop application — there is no website to block, no CEO to arrest, no server to subpoena. In the post-1099-DA world, it’s one of the few ways Americans can buy Bitcoin without a custodial broker generating a tax form on their behalf.

Note: Using Bisq does not exempt you from tax obligations. You still owe capital gains tax on profits from crypto; you just don’t receive an automatic 1099-DA. The responsibility for accurate self-reporting falls entirely on the trader.

Who it’s for: Privacy advocates; self-sovereign Bitcoin holders; users comfortable with desktop software and peer-to-peer mechanics.

Key facts:

- Bitcoin, Monero, and select altcoins

- No company, no servers, no KYC

- Fiat payment via bank transfer, Revolut, Zelle, cash by mail

- Security deposit required (BTC) to prevent fraud

- Trade volume limits per payment method

Limitation: Complexity is high; liquidity is thin compared to centralized exchanges; trade execution can take hours, not seconds.

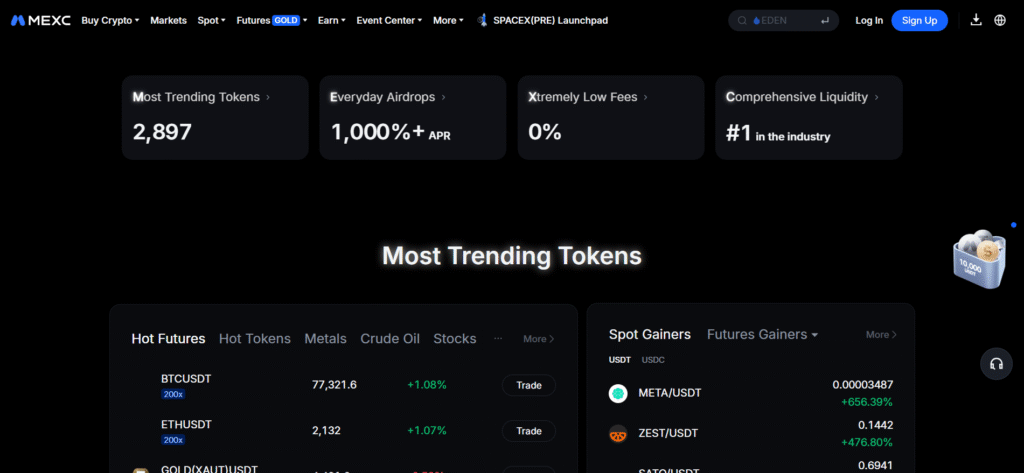

9. MEXC — High-Volume Access Without Mandatory KYC

MEXC supports over 1,600 cryptocurrencies and allows unverified users to access a significant portion of the platform — making it one of the most flexible options for traders seeking broad asset selection with minimal friction. The exchange is headquartered outside the US and is not regulated by American financial authorities. US users access it at their own legal and compliance risk; the platform itself does not explicitly block American IPs, though it disclaims compliance with US regulations.

MEXC doesn’t enforce mandatory KYC, but you need to read the fine print: the platform offers three account tiers — unverified, primary KYC, and verified plus, with a withdrawal limit of 1000 USDT per day for unverified users in most regions.

Who it’s for: Experienced traders seeking altcoin exposure beyond what US-regulated platforms offer; users comfortable with offshore exchange risk.

Key facts:

- 1,600+ cryptocurrencies

- No mandatory KYC for limited trading activity

- Spot and futures trading

- Low fees: 0% maker, 0.05% taker on spot

- Self-custody of funds recommended

Limitation: Not licensed in the US; American users take on regulatory uncertainty; limited fiat on-ramp options for US residents. As with any offshore platform, review current Terms of Service for your jurisdiction before depositing funds.

Regulated US Exchanges

All three platforms below are licensed, audited, and fully compliant with US financial regulations. They generate Form 1099-DA, require full KYC, and carry the consumer protections that come with regulatory oversight. If your priority is a fiat on-ramp, accurate tax documentation, or institutional-grade custody, start here.

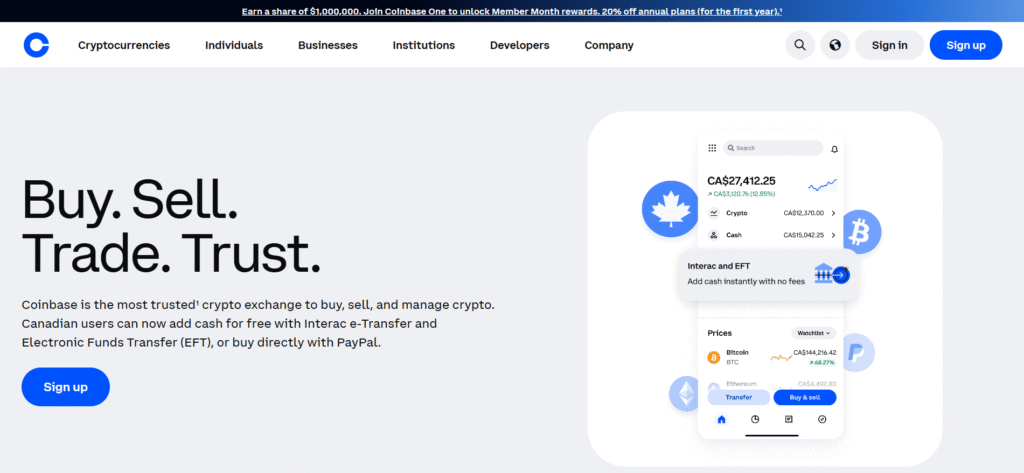

4. Coinbase — The Regulated Benchmark

Coinbase remains the most straightforward entry point for US buyers who want a fully regulated fiat-to-crypto gateway. It holds a BitLicense in New York, is publicly traded on NASDAQ, and files Form 1099-DA for every applicable transaction.

That last point matters in 2026. Starting with 2025 activity, custodial brokers report proceeds from certain digital asset sales and exchanges to both taxpayers and the IRS. Coinbase was already doing this voluntarily; it’s now mandatory. If you’re an American buying crypto and you intend to file your taxes correctly, Coinbase makes that process almost frictionless — the tax documents arrive in your account dashboard in February.

Who it’s for: First-time buyers, long-term holders, anyone who wants a regulated, auditable paper trail.

Key facts:

- Supports 270+ cryptocurrencies

- Coinbase One subscription removes trading fees

- USD cash balances held at partner banks may qualify for pass-through FDIC coverage up to $250K — note this applies to cash only, not crypto holdings

- Consistently top-rated mobile app on iOS and Android

- Full KYC required

Limitation: Spread-based fees on the standard interface can be 0.5–2%. Advanced Trade (formerly Coinbase Pro) brings this down significantly.

5. Kraken — Security-First, Battle-Tested

Kraken has operated since 2011 without ever losing user funds to a security breach — a record that speaks louder than any marketing claim in an industry that saw $3.4 billion stolen in 2025 alone. According to Chainalysis, over $3.4 billion was stolen in crypto hacks in 2025, which puts Kraken’s clean track record in sharp relief. (A 2024 zero-day exploit by a security research firm did result in $3 million being withdrawn from Kraken’s own treasury — not user funds — and the money was ultimately returned. The incident underlines Kraken’s responsiveness rather than undermining its user-safety record.)

The platform is registered with FinCEN, holds money transmitter licenses in dozens of US states, and offers both spot trading and staking. Full KYC is required for fiat deposits, but the verification process is notably fast compared to competitors.

Who it’s for: Security-conscious buyers; traders who also want access to futures and margin products.

Key facts:

- Spot, margin, and futures trading

- 300+ cryptocurrencies supported

- Competitive maker/taker fees starting at 0.16%/0.26%

- Proof of reserves published quarterly

- Support tickets typically resolved within 24 hours

Limitation: The interface can intimidate beginners; the simplified “Instant Buy” feature carries a premium over spot prices.

6. Gemini — Compliance as a Feature

Gemini, founded by the Winklevoss twins in New York, is the most compliance-forward exchange in the US — which, after the FTX collapse, is a genuine competitive advantage rather than a PR talking point.

The platform holds a trust charter from the New York State Department of Financial Services and undergoes annual SOC 2 Type 2 security audits. For institutional buyers and high-net-worth individuals navigating the post-1099-DA world, Gemini’s ActiveTrader interface and custody solutions are worth serious consideration.

Who it’s for: Institutional buyers, high-net-worth individuals, traders who prioritize regulatory certainty.

Key facts:

- 100+ cryptocurrencies

- Completed IPO in late 2025 (trades as GEMI on public markets)

- Insurance coverage on custodied assets

- Gemini Pay for real-world crypto spending

- Full KYC required

Limitation: Smaller selection of altcoins compared to global exchanges; fees on the basic interface are among the highest in the industry.

Mobile Apps & Everyday Buyers

These apps are designed for people who want crypto exposure without switching platforms or learning to trade. All three are US-regulated, support fiat deposits, and are built to be used on a phone rather than a trading terminal. None is the right tool for deep altcoin selection or active trading — but that’s not what they’re for.

7. Robinhood Crypto — Zero-Fee Simplicity

For buyers who already use Robinhood for stocks and want to add Bitcoin or Ethereum without opening a new account, Robinhood Crypto delivers one of the most frictionless fiat-to-crypto experiences available to US residents. Trades execute commission-free; the interface is clean enough for a 10-year-old; and crypto lives inside the same app as your equity portfolio.

The catch: Robinhood holds your crypto in a custodial account. You couldn’t withdraw to an external wallet until 2022 — they eventually added that feature, but self-custody still isn’t the ethos here.

Who it’s for: Stock investors who want a small crypto allocation without complexity; mobile-first buyers.

Key facts:

- 20+ cryptocurrencies (smaller selection)

- No explicit trading commissions — revenue comes from the bid-ask spread

- Instant bank deposits up to $1,000

- Crypto transfers to external wallets supported

- ETH, SOL, and ADA staking available in-app

- Full KYC required

Limitation: Limited coin selection; spread-based pricing isn’t always transparent about what you’re actually paying per trade.

8. Crypto.com — Broad Selection, Competitive Rates

Crypto.com has built one of the widest crypto selections available to American users, with over 350 assets and a tiered rewards system tied to its CRO token. The platform holds a Money Services Business license with FinCEN and holds state-level money transmitter licenses across most of the US.

The Crypto.com Visa card offers cashback ranging from 1% to 5% depending on how much CRO you stake, with a headline 8% tier that requires approximately $400,000 in CRO locked for 180 days — an outlier, not the typical user experience. Most users land in the 1–3% range. The card has attracted a retail audience that treats crypto as an everyday spending tool; the rewards are real, but the tier structure rewards those already deep in the ecosystem.

Who it’s for: Active traders who want rewards and a broad asset selection; users who want a crypto debit card.

Key facts:

- 350+ cryptocurrencies

- Visa card with 1–5% cashback in CRO (tier depends on CRO staked; 8% maximum requires ~$400K stake)

- DeFi wallet integration

- Full KYC required after a low-volume trial tier

Limitation: The best rates and card benefits require staking significant amounts of CRO; complex fee structure.

9. Cash App — Bitcoin the Simple Way

Cash App by Block (formerly Square) is the easiest way to buy Bitcoin with dollars in the United States — period. You fund it from your bank account, tap Buy, and you own Bitcoin. The platform supports auto-buy (daily, weekly, or bi-weekly), making it a practical tool for dollar-cost averaging.

Bitcoin-only. That’s the limitation. If you want Ethereum, Solana, or anything else, Cash App won’t help you. But for people whose entire thesis is “own some Bitcoin every month, no complexity,” it’s unmatched.

Who it’s for: Bitcoin-only buyers who want maximum simplicity and DCA automation.

Key facts:

- Bitcoin only

- Instant deposits via linked debit card

- Automatic recurring buys (DCA-friendly)

- Bitcoin withdrawals to self-custody supported

- Fee: 1.75% per transaction (or a flat minimum fee)

Limitation: Single asset only; not a platform for portfolio diversification.

Physical Cash Access

For users who want to convert paper money to Bitcoin without a bank account, a card, or any online account, Bitcoin ATMs are the most direct option. They are also the most expensive.

10. Bitcoin ATMs — Cash-to-Crypto, No Bank Required

Bitcoin ATMs allow US residents to buy Bitcoin (and sometimes other cryptocurrencies) with physical cash — no bank account, no credit card, no ACH delay. The US hosts around 30,000 of these machines, though the network has been contracting in 2026 as regulatory pressure squeezes operators and the sector’s largest provider, Bitcoin Depot, filed for bankruptcy in May 2026. Availability remains broad but should be verified locally before making a trip.

The trade-off is price. ATM operators typically charge 8–20% above spot price, making them the most expensive option on this list by a significant margin. KYC requirements vary: many machines allow purchases under $900–$1,000 with just a phone number; amounts above certain thresholds require ID scanning per FinCEN anti-money-laundering rules.

Who it’s for: Unbanked users; people who want to pay with cash; buyers in areas with poor banking access; small one-time purchases.

Key facts:

- Available in most US cities, many 24/7 — use Coin ATM Radar to find machines near you

- Bitcoin primarily; some machines support ETH, LTC, DOGE

- Cash purchases under ~$900 often require only a phone number

- No account creation needed

- Instant transaction, funds sent to your wallet

Limitation: Fees are extremely high (8–20%); limits per transaction; machine availability varies by location.

The 1099-DA Landscape: What It Actually Means for You

Form 1099-DA is the IRS information return used to report digital asset sales and exchanges through custodial brokers, applying to 2025 transactions with forms generally furnished to taxpayers in 2026. If you use Coinbase, Kraken, Gemini, Robinhood, or Crypto.com, you will receive one of these forms. That’s not a reason to panic — it’s simply how the system now works, similar to how your stock broker sends you a 1099-B.

Whether or not you receive a Form 1099-DA, you must report all income, gains, and losses from digital asset transactions on your federal income tax return. The form is a reporting mechanism, not an automatic tax bill. You owe tax only on realized gains; losses offset those gains.

Three important points for 2026:

- Cost basis reporting begins this year. Starting January 1, 2026, brokers are required to report the cost basis of digital assets — that is, the original value of the asset for tax purposes. This means your 1099-DA (for 2026 transactions) will include both proceeds AND cost basis for the first time.

- Non-custodial platforms are outside scope. The form does not cover purely on-chain swaps, smart-contract interactions, or other DeFi-native mechanics when they occur outside a custodial broker environment. Platforms like Bisq and Godex don’t generate 1099-DAs because they’re not custodial brokers. You still owe tax on any gains — you simply report them yourself.

- Keep your own records regardless. Cross-reference any 1099-DA you receive against your own records. The form may omit transfers between wallets or exchanges, which can artificially inflate reported proceeds.

This is not financial or tax advice. Consult a qualified CPA or crypto tax professional for guidance specific to your situation.

How to Choose: A Quick Decision Framework

Not all ten platforms above suit all users. Here’s a practical filter:

“I’m buying crypto for the first time with dollars.” → Coinbase, Robinhood, or Cash App (Bitcoin only). All three are built for people who don’t want friction.

“I want the widest asset selection and lowest fees.” → Kraken (Advanced) or Crypto.com. Both offer deep markets and tiered fee structures.

“I already own crypto and want to swap without KYC or registration.” → Godex. Non-custodial account model, no data retained, fixed or floating rate, BTC, privacy coins, altcoins, and niche tokens all covered.

“I want to buy Bitcoin as privately as possible.” → Bisq (most private, P2P) or Bitcoin ATMs (cash, with minor phone verification for small amounts).

“I want access to obscure altcoins US-regulated exchanges don’t list.” → MEXC. Understand the offshore risk before proceeding.

“I’m an institution or a high-net-worth buyer who needs audit-grade compliance.” → Gemini. SOC 2 certified, trust chartered, custody insurance.

What to Watch in the Second Half of 2026

The regulatory picture is still moving. The SEC’s recent dismissal of multiple cases against crypto exchanges has taken some pressure off the industry, while the DOJ stays focused on clear misconduct. Broader market structure legislation (defining whether tokens are securities or commodities) is expected to pass or stall in this Congressional session, with real downstream effects on which platforms can legally operate for US customers.

A few trends to track:

- More offshore exchanges will geo-block US IPs. Platforms that have been passively allowing American users without a US license will face increasing pressure to choose: register or restrict. Expect the list of accessible no-KYC offshore platforms to shrink further.

- DEXs and non-custodial tools will gain users. Every time a major CEX collapses or implements unexpected KYC demands, some portion of its users migrates to self-custodial alternatives. The FTX legacy accelerated this trend; the 1099-DA rollout is accelerating it further.

- Tax enforcement may intensify. The IRS is already cross-referencing 1099-DA data with blockchain analytics tools. Users who bought on Coinbase, transferred to a Ledger, swapped on a non-custodial platform, and never reported the gain are increasingly exposed. The paper trail is longer and more connected than most people realize.

The Bottom Line

The ten platforms above cover the full spectrum of how Americans can access crypto in 2026 — from the fully regulated and tax-reporting (Coinbase, Gemini, Kraken) to the private and non-custodial (Bisq, Godex, Bitcoin ATMs). None is universally “best.” Each occupies a different position on the compliance-privacy-convenience triangle.

What’s changed in 2026 is the stakes. The 1099-DA makes custodial exchange activity visible to the IRS by default. The FTX bankruptcy and criminal fraud conviction reminded everyone what counterparty risk looks like. And the SEC’s recalibrated enforcement posture — focused on genuine fraud rather than regulatory grey zones — has created more breathing room for legitimate platforms of all types.

Whatever your approach, the fundamental principle remains unchanged: understand where your keys are, understand what data is being collected, and keep your own records. The platform is just the tool. The responsibility is yours.

Frequently Asked Questions (FAQ)

If I swap on Godex, do I still owe taxes or does no-KYC mean no taxes?

No-KYC doesn’t mean no-tax — it means no automatic paperwork sent to the IRS on your behalf. You still owe capital gains tax on every profitable swap; the difference is that Godex doesn’t generate a Form 1099-DA, so the reporting responsibility falls entirely on you. Keep your own records: which pair you swapped, the date, the amounts, and the approximate USD value at the time. Ignoring the tax obligation because no form arrived is the mistake that gets people in trouble when IRS blockchain analytics tools cross-reference on-chain data.

Is a no-KYC swap platform actually legal in the USA?

Using a non-custodial instant swap service like Godex is not illegal for US residents — it’s the same legal category as using a DEX. The platform operates outside US jurisdiction, doesn’t hold your funds, and doesn’t function as a registered broker, so it falls outside the scope of US broker regulations. What remains your legal responsibility regardless of platform: accurate self-reporting of gains on your federal tax return. The platform being legal and your tax obligations being real are two separate questions; don’t confuse one for the other.

Can the IRS actually see what I do on a no-KYC platform?

The IRS doesn’t receive a direct report from non-custodial platforms, but that doesn’t make the activity invisible. Blockchain transactions are public by design — every Bitcoin or Ethereum move is permanently recorded on-chain. The IRS uses blockchain analytics vendors like Chainalysis to trace fund flows, and if your crypto ever touches a regulated exchange (to cash out, for example), that connection gets made. Privacy coins like Monero are harder to trace, but even those have on/off-ramp exposure points. Treating non-KYC as equivalent to untraceable is a bad assumption.

Coinbase fees are insane. Is there a cheaper regulated option?

Coinbase’s standard interface uses spread-based pricing that can cost 0.5–2% per trade — yes, that’s genuinely high. Switch to Coinbase Advanced Trade (the same account, different interface) and fees drop to 0.6% taker / 0% maker at entry level. Alternatively, Kraken charges 0.26% taker on spot trades and is also fully regulated and US-licensed. If you’re dollar-cost averaging small amounts, the flat minimum fee matters more than the percentage — run the numbers before assuming one platform is always cheaper.

Why not just use Uniswap instead of an instant swap service like Godex?

Uniswap is great for ERC-20 token swaps within Ethereum’s ecosystem, but it doesn’t natively handle cross-chain swaps — you can’t go from BTC to XMR or SOL to ADA without bridges and multiple steps. Godex handles hundreds of cross-chain pairs in a single transaction with a fixed rate, no wallet connection required, and no gas fee management on your end. If you’re already inside one chain and trading tokens on it, Uniswap works well. If you need to move between chains or access privacy coins, an instant swap service is the cleaner path.

This article is for informational purposes only and does not constitute financial, tax, or legal advice. Cryptocurrency trading involves significant risk. Tax obligations vary by jurisdiction and individual circumstance — consult a qualified professional before making trading or tax decisions.

Start a Cryptocurrency exchange

Try our crypto exchange platform

Disclaimer: Please keep in mind that the content of this article is not financial or investing advice. The information provided is the author’s opinion only and should not be considered as direct recommendations for trading or investment. Any article reader or website visitor should consider multiple viewpoints and become familiar with all local regulations before cryptocurrency investment. We do not make any warranties about reliability and accuracy of this information.

Read more

EOS is definitely on the list of the strongest and most stable projects in the crypto world. Despite the fact that the currency entered the market less than 3 years ago, it consistently occupies one of the top 10 places in the rating for project capitalization. it is often called the “main competitor of Ethereum”. […]

XRP price prediction 2026-2027: bear, base, and bull scenarios with ranges and named sources, the resolved SEC case, live spot ETFs, and can XRP reach $10?

In this article we will talk about Ripple (XRP) and its price prediction. What is Ripple (XRP) Ripple is a San Francisco-based startup that was launched in 2012 by Ripple Labs as a global network both for cross-currency and gross payments. Ripple history began in 2004 with the discussions around the digital coin in the […]

You may well think that an article dedicated to a Tether price prediction or the Tether price in general is a little bit strange — it is a stablecoin after all. However, the price of Tether does fluctuate significantly, although it is nowhere near as volatile as non-stablecoin cryptos. This means that staying up to […]

In the article we share our vision at Zcash cryptocurrency main features and add several price predictions. As cryptocurrencies gain global acceptance and decentralisation slowly enters our lives, privacy becomes the main concern when talking about blockchain adoption. It is no secret that distributed ledger is by far the most secure and transparent technology ever […]

Chiliz coin (CHZ) offers a compelling opportunity for traders interested in the intersection of blockchain technology and sports. By enabling fans to influence team decisions through the Socios app, Chiliz directly monetizes fan engagement and connects with major sports teams like Juventus and Paris Saint-Germain. These partnerships not only enhance the platform’s visibility but also […]